Dear Capitolisters,

Last week, U.S. Steel announced that it was canceling a $1.3 billion upgrade to its Mon Valley Works plant in Pittsburgh, Pennsylvania—a project that was widely praised at the time of announcement in May 2019 as proof that President Trump’s steel tariffs were “working.” (Trump himself tweeted as much back when he, ya know, could do that.) Given the pandemic and other recent events, as well as hints from U.S. Steel itself last year that the Pittsburgh project’s fate in question, the announcement wasn’t exactly surprising, so I was content to fire off a couple snarky tweets (as one does) and move on. But then this tweet from American Compass’ “free market fails” project came across my screen:

As anyone who follows the issue knows, it’s pretty preposterous to assert that U.S. Steel’s decision to bail on the Mon Valley Works project is a clear failure of “American capitalism” and a sign of the free market’s bigger investment problems. But this tweet does provide us with a great opportunity to discuss both the history of the U.S. steel industry and the industrial policies that have long supported it, and the broader genre of analysis on the left and (increasingly) the right that blames any and all adverse events on “market failures” necessitating new government action.

So let’s dig in, shall we?

Our Long History of Supporting Big Steel

Before we get to last week’s announcement, it’s important to first get caught up on the United States’ long and ignominious history backing “Big Steel,” the most prominent member of which is U.S. Steel. As I explained in a 2017 paper and several subsequent articles, U.S. steel companies and workers since the 1970s have probably received more government assistance than any industry in the country. This includes hundreds of import restrictions; tens of billions of dollars in state, local and federal subsidies and bailouts; exemptions from environmental regulations; special “Buy American” rules just for integrated steelmakers like U.S. Steel; and federal pension benefit guarantees.

Big Steel has earned these goodies through its intensive lobbying efforts and strong ties to the U.S. government. There’s a large “Steel Caucus” in both chambers of Congress, and the executive branch usually harbors similar fans. This coziness likely reached its zenith during the Trump years, as several of the Trump administration’s top officials—including U.S. Trade Representative Robert Lighthizer (and several of his deputies), Commerce Secretary Wilbur Ross and White House Director of Trade and Manufacturing Policy Peter Navarro—had close connections to Big Steel.

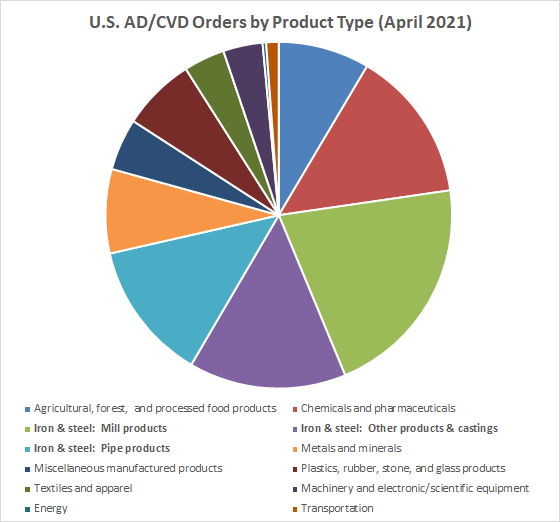

These connections’ results, especially on the trade front, are nothing less than breathtaking. As of last week almost half (292) of the 599 current U.S. “trade remedy” (anti-dumping and countervailing duty) orders, which impose duties on certain “unfairly traded” products from specific countries (using increasingly dubious methodologies to do so), are on iron and steel products:

As I explained in a recent blog post, economic studies show that these duties have had large, negative effects on downstream U.S. industries in terms of increased production costs and decreased employment, wages, sales, and investment, but had no significant effect on blue‐collar jobs, wages, or sales in the protected industries (even though the duties decreased imports and increased foreign and domestic prices). There’s also ample evidence that many of the steel import duties were politically motivated (shocking, I know)—the result of a “captured” Department of Commerce and the repeated efforts of Big Steel’s advocates in Congress to tilt the legal playing field in their benefactors’ favor.

Those same members are now itching for more. Such are the perils of policing “unfairness”—it means whatever the law-writers (and their most, ahem, eager supporters) want it to mean.

Then, of course, there are the 25 percent “national security” tariffs that President Trump imposed on almost all steel products in 2018 (at the request of U.S. Steel and other large producers). As I explained earlier this year, the tariffs’ imposition was wholly unjustified:

-

Prior to the tariffs’ imposition, the U.S. steel industry had already won billions of dollars in government subsidies and import protection through dozens of U.S. trade remedy measures covering almost 61 percent of all steel product imports in 2017, the year before the Section 232 tariffs took effect.

-

Data in Commerce Department’s own Section 232 report showed that the steel industry was at no risk of collapse and instead had steady steel output (about 80 million metric tons) and production capacity (about 115 million metric tons), a still-dominant 70 percent domestic market share, and solid financials.

-

Imports posed no immediate threat to the United States’ ability to procure steel for national defense needs because the vast majority from “reliable” (in Commerce Department parlance) U.S. allies, such as Canada (the largest source country), Brazil (2), South Korea (3), Mexico (4), Japan (7), and various EU countries. Meanwhile, China—the repeated excuse for the Section 232 tariffs—was only the 11th largest U.S. supplier of steel in 2017, suffering a 31 percent drop since 2011 (due in part to the aforementioned U.S. trade remedy measures).

-

A statutorily required assessment from then‐Secretary of Defense James Mattis found that broad tariffs weren’t needed: “the U.S. military requirements for steel and aluminum each only represent about three percent of U.S. production … DoD does not believe that the findings in the [Commerce Section 232] reports impact the ability of DoD programs to acquire the steel … necessary to meet national defense requirements.”

These facts and Mattis’ recommendations, of course, were ignored. Instead, President Trump—at a photo-op meeting with U.S. Steel’s CEO, other steel executives, and union leaders—announced in March 2018 blanket 25 percent tariffs (inexplicably 1 percentage point higher than what the Commerce Department recommended) on all types of steel, including commodity products (e.g., rebar) with little national security nexus, semi-finished products (e.g., slab) that American steel companies needed to maintain their domestic operations, and steel from close U.S. allies such as Canada, Japan, the EU, and U.K.

As we’ve discussed here repeatedly, the Section 232 tariffs caused U.S. steel prices to spike, harming most domestic manufacturers but providing windfall profits to U.S. Steel and a few other large producers—producers who continuously lobbied to keep the tariffs in place and deny hundreds of U.S. importers any exemptions therefrom. Today, steel prices are through the roof, harming the manufacturing sector and threatening the nation’s economic recovery. The tariffs also are causing geopolitical headaches for the Biden administration and have done little to change the industry’s overall trajectory.

Yet they remain in place—a testament to Big Steel’s political might and the unfortunate staying power of bad industrial policy.

So What Really Happened with U.S. Steel?

And that brings us to U.S. Steel, whose decision to ditch Mon Valley Works project was not a “market failure” at all and instead a textbook case of protectionism doing what protectionism does.

Based on various reports and the CEO’s own comments on the company’s latest earnings call, the company abandoned the project—and also announced curtailments at a nearby coke facility—for several reasons. For example, Pittsburgh-area politicians, labor unions, and business organizations blamed long delays in the permitting process for scuttling the plant: Even as the pandemic waned and a rival steel project got off the ground, the company’s permits still hadn’t been approved. Another strike against the project was that the facilities used old, carbon-intensive technology (blast furnaces and coke to fuel them) that worked directly against the company’s new goal to dramatically reduce greenhouse gas emissions. (Some of the equipment at issue had long been “criticized as among the area’s worst polluters.”) Neither of these issues could possibly be considered a failure of free market capitalism.

Most importantly, however, is the fact that, only a few months after making the Mon Valley Works announcement, U.S. Steel acquired a big stake in a cleaner and more efficient “mini-mill” in Arkansas:

For 118 years, U.S. Steel has been the face of the age-old blast furnace, becoming a giant in the industry by reliably melting, casting and pouring steel from scratch at integrated mills like the Mon Valley Works.

Now, in the middle of yet another downturn in steel prices, the Pittsburgh steelmaker is embarking on perhaps its biggest shift in strategy — organizationally, culturally, geographically — in that long history. The company is staking its future on a lower-cost Arkansas minimill, which uses electricity to melt recycled scrap metal and is backed by Koch Industries.

The company initially bought a 49.9 percent stake of Big River Steel but upped that to 100 percent in January. Even in 2019, this acquisition was the writing on the wall for Mon Valley Works because the Big River mini-mill was not only more efficient and environmentally-friendly than the old-school blast furnaces in Pittsburgh, but also non-unionized:

The Arkansas plant, like so many others constructed more recently in Southern states, employs nonunion workers. Manufacturing in general has moved from the industrial Midwest and away from the influence of labor unions.…

Arkansas has a right-to-work law, which means any employee can opt out of joining and paying dues to a labor union. Right-to-work laws make it difficult for unions to organize local chapters and bargain contracts. …

Meanwhile, the Mon Valley Works’ efficiency upgrades are widely expected to gradually cost jobs through attrition, as two distinct parts of the complex merge into one.

This acquisition allowed the company—even at a time of insanely high prices—to avoid making any additional capital expenditures and instead simply take the crazy profits (made even crazier by Big River’s efficiencies) that the current, protected market was giving them. And several U.S. Steel executives basically admitted as much on the company’s latest earnings call, in which they repeatedly trumpeted Big River Steel’s profitability and their “value creation” for shareholders, and said they had no intention of increasing capital expenditures or bringing any idled Midwest capacity back online in the face of record high demand (and prices), choosing instead to reap “outsized returns.” Quoth those same executives:

At Big River Steel, it’s not just about how much steel you can make, it’s about how much money you can make per minute of the line time.… [W]e will continue to run Big River prioritizing profitability per minute on the line to ensure we’re driving the right margin performance, the right EBITDA [earnings before interest, taxes, depreciation and amortization] per ton performance and continue to generate value from that asset.

Now, as a committed “free market fundamentalist” (lol) I have little problem with a private company emphasizing efficiency, profitability, and shareholder value as it operates in a relatively free market, but that is of course not the situation we have here. Instead, we have a government-created oligopolist pocketing rents and boosting its executives’ and shareholders’ wallets instead of investing in new technologies, hiring more workers, or even boosting pre-existing (idled) capacity—precisely what the economics literature anticipates and what we’ve seen with past episodes of American steel protection.

For example, my 2017 paper details what steel protection in the 1980s (emphasis mine) did to the industry’s investment and innovation:

A 1986 report from the CBO considered the effects of trade protection in revitalizing domestic firms in four cases—textiles and apparel, steel, footwear, and automobiles—between the 1950s and 1970s. The authors found that, indeed, U.S. trade barriers limited imports and increased protected firms’ output, employment, and profits above what they would have been without protection. However, “[i]n none of the cases studied was protection sufficient to revitalize the affected industry.” The steel, footwear, and textile and apparel industries repeatedly sought new import protection after their previous protection expired, and the automobile industry succumbed to imports of the small cars that were the source of their “competitive difficulties.” Furthermore, the protection did not significantly increase the companies’ incentive to invest in cost-saving technologies that would improve their long-term competitiveness— even when the protected companies had the capital available to make such investments. The authors concluded that, because the system of trade restraints was unable to save protected industries, the U.S. government should consider policies other than import protection—such as encouraging investment in less labor intensive industries, aiding displaced workers, or ending “special treatment for trade-impacted industries”—when crafting new U.S. trade policies….

A 1987 study from Robert Crandall on “The Effects of U.S. Trade Protection for Autos and Steel” found that this protection limited imports but actually harmed the industries’ long-term position. For example, it discouraged improvements in product quality and encouraged cannibalistic overinvestment and too-rich labor contracts that “simply postpone[d] part of the necessary adjustment to the loss of competitiveness.” As a result, Crandall concluded, “The experience with the auto and steel industries raises serious questions about the effectiveness of quotas as a means to revitalize an industry.”

Though these restrictions didn’t lead to more jobs or greater investment, GWU’s Susan Aaronson recalls that they did produce one clear winner:

Protectionism, we found, was not the answer: It did little to encourage managers at many firms to modernize and invest in their employees. With imports at higher prices (through tariffs and quotas), steel industry executives used the breathing room from protectionism to increase returns to shareholders or to attract buyers for their firms. So protectionism was not only costly to consumers, it didn’t preserve jobs or firms.

Subsequent research from the Mercatus Center also shows that trade remedies protection (which, again, overwhelmingly benefits Big Steel) also padded company executives’ pockets: “Research shows that import duties such as tariffs consistently cause hikes in executive pay that cannot be explained by company or CEO performance.”

Thus, far from being some sort of “market failure,” the U.S. Steel situation—and similar profit-taking by its Big Steel colleagues—is just par for the protectionist course. By contrast, research shows how imports and foreign competition can act as an important check on U.S. manufacturers’ market power, and can push them to upgrade productivity and increase innovation. Engaging in trade and global supply chains also can boost both domestic firms’ productivity and economic growth more broadly. So if we want to see U.S. Steel investing and innovating again, probably the best thing we could do is to lift the tariffs and let competition do its thing.

Market Failures Everywhere

Big Steel’s recent actions are a great example of not only the unintended consequences of protectionism, but also alleged “market failures” actually caused by bad government policy. Other examples of this latter point abound – in just the last few weeks, people have blamed government inaction for skyrocketing lumber prices, while ignoring the short- and long-termeffects of the almost-four decades of U.S. government protection from and managed trade of lumber from our largest import supplier, Canada (as well as other policies here and in Canada that limit supplyanddemand). Likewise, the global semiconductor shortage has been pinned on free markets and a lack of government planning, ignoring (among other things) how – as we’ve discussed – U.S. export controls exacerbated the situation. And then, of course, there’s health care and education and housing and …

You get the idea.

In most of these cases, forces other than government meddling are undoubtedly contributing to the price and supply issues hitting the U.S. market. (That’s certainly the case for lumber and semiconductors right now.) And market failures do occasionally happen. Often, however, only a couple of these forces are under policymakers’ control, and removing these policy own-goals should be considered priority one when formulating new policy responses, lest those responses simply pile distortions on top of distortions instead of actually fixing the situation.

This reality also argues for more caution and humility about calling every problem in the U.S. economy—real and imagined—a failure of the free market modern capitalism. Often, the failure lies not in a lack of intervention, but in the intervention that’s already there.

Conservatives used to get this. Do they still?

Chart(s) of the Week

The state of the U.S. labor market as of March 2021 (source):

The Links

Me on the rhetoric and reality of “middle class tax hikes” (Plus recent testimony on supply chains and small manufacturers)

Please note that we at The Dispatch hold ourselves, our work, and our commenters to a higher standard than other places on the internet. We welcome comments that foster genuine debate or discussion—including comments critical of us or our work—but responses that include ad hominem attacks on fellow Dispatch members or are intended to stoke fear and anger may be moderated.

With your membership, you only have the ability to comment on The Morning Dispatch articles. Consider upgrading to join the conversation everywhere.